The End of Fragmentation

Why AI will consolidate markets and create the biggest businesses of all time

Many people seem to have the intuition that AI will fragment markets.

The thinking is that because it is now much easier to create software, new companies will be built to serve every niche use case and low-TAM market. Clones of major tech companies will emerge to carve out market share.

This is similar to the intuition people had about the internet, and they were wrong then too.

AI will drive greater concentration of value into fewer companies and create the biggest businesses of all time.

This essay is a brief exploration into why and how this will happen.

The historical trend

The economy is on a long arc toward concentration. We started with small shops in every town and ended up with Amazon. We started with millions of local musicians and ended up with Taylor Swift.

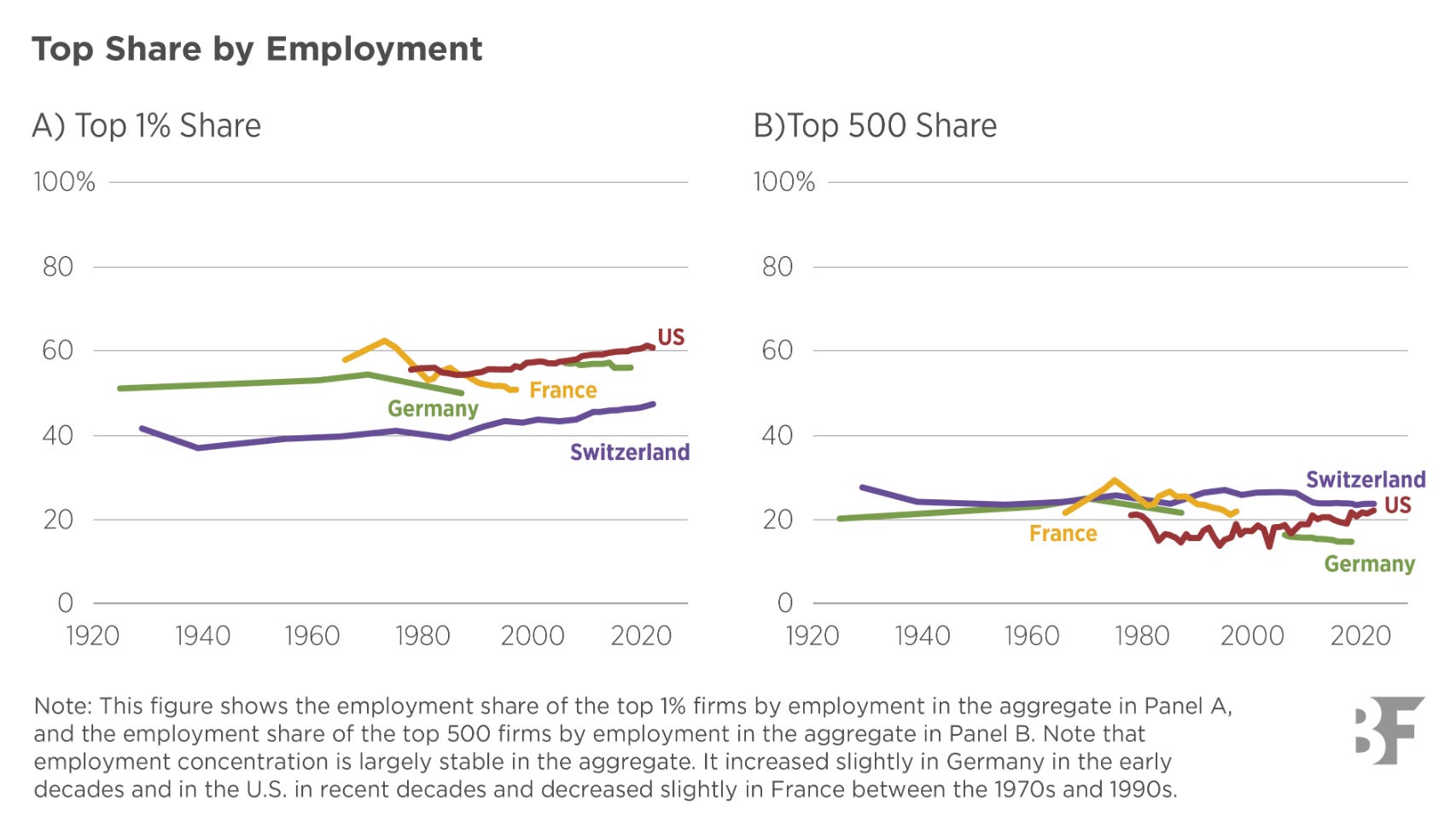

For at least the last 100 years, this has been a trend toward concentration of value (revenue, profit, capital) into the top companies, but not a concentration of labor.

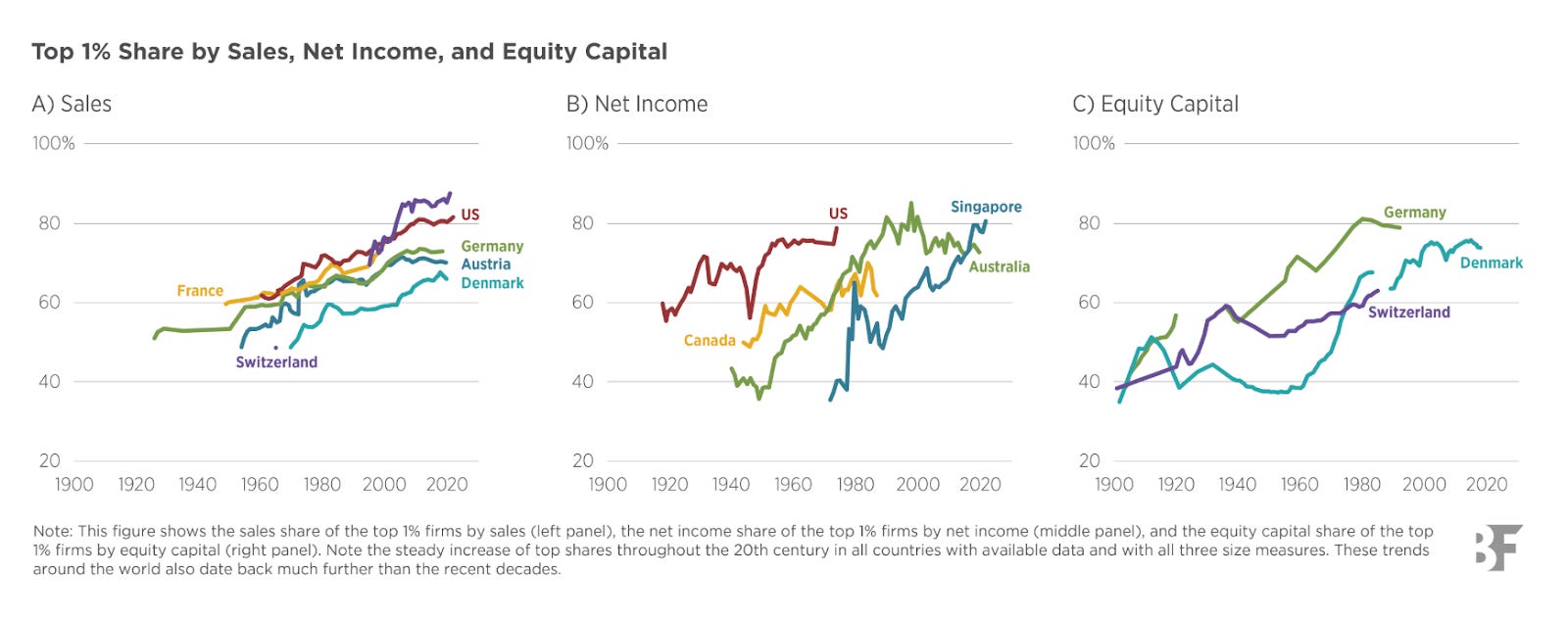

A recent study demonstrated that the share of value accruing to the top 1% of companies has steadily increased since the early 1900s, and is now at about 80% across most major market economies.

Over the same period, however, the share of employment in those top firms has been essentially flat.

This divergence between value and labor helps to explain why many people got the internet wrong. It did, in fact, enable the creation of many more small businesses in industries like consumer products, retail, media, and services. This was decentralizing in many visible ways: more entrepreneurs, more startups, and greater diversity in the products and media we consume.

But over the same period, concentration of value just continued to march upward. One reason for this is that while the internet enabled a wave of small businesses, it also enabled a new kind of mega-company, which Ben Thompson called the aggregator. Companies like Google, Meta, and Apple control the distribution that all of these new businesses need in order to grow, and as a result, command much of the newly generated economic value.

Why AI will accelerate this trend

There are two mechanisms by which new technology has consistently driven greater concentration, and AI will reinforce both.

The first driver of concentration is that technology increases the power of the leading companies relative to their competitors.

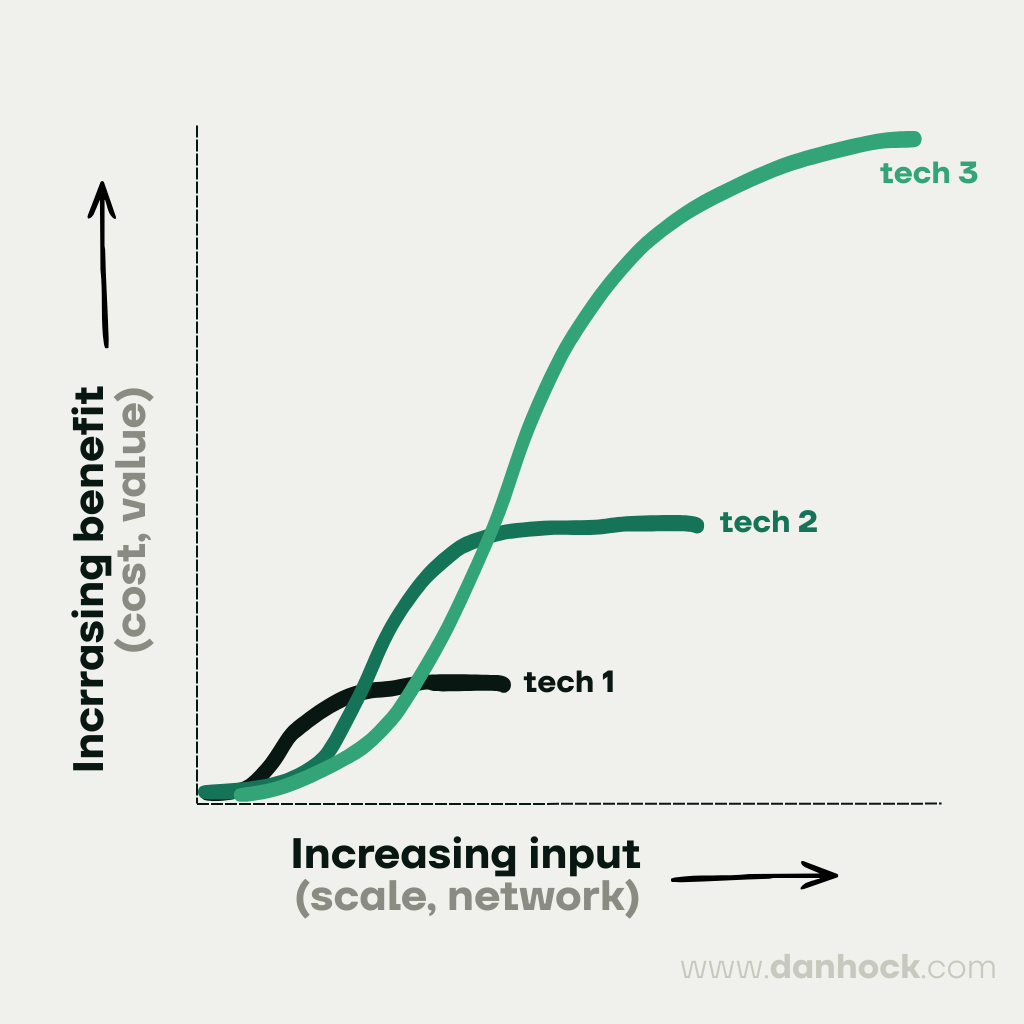

Power (sometimes called defensibility) is the ability for a company to durably earn more than its competitors. You can represent it with an s-curve, with an increasing input (scaling operations, growing customer network) on the x-axis and an increasing benefit (lower costs, more valuable product) on the y-axis.

Technology tends to push this curve outward: the top companies now have farther to move along the curve before the benefit asymptotes, making it harder for anyone to catch up. Technologies like manufacturing and the semiconductor pushed the curve out for scale economies. The telephone and the internet pushed it out for network effects.

Certainly for chip manufacturers, and probably for the frontier model companies, the scale economies curve has again shifted out. At this point, it’s difficult to imagine anyone but an incumbent with existing scale entering the competition.

For the application layer of AI, the change will come in the form of strengthening data effects, where the larger and more proprietary the dataset, the more value a product can deliver.

Prior to AI, data effects came in a milder form: Amazon’s product ranking improving with more conversion data, Stripe’s fraud model getting better with more transactions. These are powerful but have capped upside on the y-axis: purchase conversion or fraud prevention can only get so good.

The data effects of AI applications will be different for two reasons. First, they don’t just optimize the product; they determine what it is capable of doing in the first place. A moderate amount of tax return data might allow a company to build a pretty good CPA assistant. But a lot of tax return data may mean they can just close the books and file returns for any small business in the US. Second, the data produces a generalizable capability: that same tax return data may mean the company can also underwrite any SMB in the country for a new credit line.

The second driver of concentration is that technology lowers transaction costs within companies.

In The Nature of the Firm, Ronald Coase answered the question: why do we need companies at all? If the free market is so good at allocating resources via prices, why don’t individuals just contract with each other for every task?

His answer: coordinating each transaction has a cost (setting a price, negotiating, enforcing contracts), and companies can lower these costs by coordinating them internally. In most cases, for example, it is more efficient to hire a marketer than to contract out each marketing task to a 3rd party.

Why, then, isn’t the whole economy just one big company? Because as you organize more activity within a company, it starts to get too complicated, and resources start getting allocated inefficiently. From Coase:

“Other things being equal, therefore, a firm will tend to be larger:

a. the less the costs of organizing and the slower these costs rise with an increase in the transactions organized.

b. the less likely the entrepreneur is to make mistakes and the smaller the increase in mistakes with an increase in the transactions organized....

This isn’t just theory - if you’ve spent any time around big companies, you’ve felt it viscerally. As companies grow, they start to trip over themselves. There are too many people and too much process. This is when companies start failing to make the next leap into a new product extension or market expansion. This is when they start hiring vendors and consultants instead of doing things themselves, because it’s easier to just over-pay instead of wading through the internal molasses.

Technology often helps with this problem. Software like Excel, Salesforce, Notion, or Slack makes it easier for companies to manage themselves, and in effect raises the size of the team or level of complexity at which the company becomes unmanageable.

AI will do this much more powerfully than legacy software, because it won’t just give humans tools to manage more efficiently, it will do a lot of the work itself. AI means many fewer people will be required to produce a unit of output. This will lower headcount, lower complexity, and cause internal coordination costs to plummet.

In the process, it will make companies much more valuable per employee, which will allow them to retain their best people by both paying them more and creating an environment in which they can actually get things done. It will take longer before a company’s best people start jumping ship for somewhere with less bureaucracy and more upside.1

The combination of these two drivers means that both companies have more to gain from getting larger, and they will be able to get much larger before they become slow, dumb companies and start making mistakes.

These dynamics will concentrate more value into fewer super-companies, a dynamic that will play out from two directions: (1) consolidation of existing software companies and (2) turning non-software industries into software and consolidating them in the process.

Software consolidation

The average large company in the US runs about 350 different SaaS apps.2 That number is about to come down a lot.

It would be advantageous for a software company to use a shared infrastructure and data model to address a wide range of use cases. But so far, they have been held back from becoming massively multi-vertical by three things:

The sheer volume of software to build and maintain

The difficulty in understanding the needs of many different kinds of customers and use cases

The inability to expand without creating a product that is much too complicated for the typical user to navigate

AI weakens all of these constraints. The first is the most obvious: coding agents dramatically reduce the cost of building software. And they won’t just ship the initial product; they will also help to respond to and adapt it to bugs, edge cases, and feature requests.

Second, it will now be easier for one company to maintain more high-quality product teams. Previously, creating a new product pod might have meant hiring 10-12 people. Soon it might mean hiring 3-4. And as we discussed above, it will be more feasible for companies to retain their very best PMs, designers, analysts, and engineers who are doing the hard work of customer needs finding.

Finally, there will be agents running on top of all of the software that is built. Instead of users drowning in a growing sea of menus, settings, and workflows, they will have a simple entry point. Agents will abstract the complexity away when they don’t want it, and direct them to the correct workflow when they do.

As a result, we’ll start seeing companies jump across functional and industry lines that used to look static. Do you really need Workday as the system of record, Greenhouse for recruiting, Lattice for performance management, Culture Amp for employee engagement, Pave for compensation, and Checkr for background checks? Why isn’t that all just one thing?

It’s hard to tell who will do this consolidation — probably some mix of software companies expanding horizontally into new use cases, frontier models expanding downward into apps, and PE rolling up struggling software businesses. But no matter who does it, consolidation among existing companies is coming.

You might be thinking that this makes sense for existing players, but what about the long tail of new software companies that just couldn’t be built before AI and now will? Won’t those drive fragmentation?

I’m not convinced that small-TAM software will be built by individual companies. It might be that multi-vertical software businesses expand into ever-narrower use cases. But it’s certainly possible that there is just such a long tail of use cases that big companies can’t serve them well, and a wave of new entrepreneurs and companies do emerge to serve them.

If this happened, however, it would follow a pattern similar to what we saw in media, consumer products, and online retail during the rise of the internet: an explosion of many new companies driving the number of new firms up, but the bulk of value accruing to the aggregators who own distribution.

That is because AI will make it easier to build, but it will not make it easier to get distribution, and that will become the bottleneck, allowing aggregators to extract most of the value.

In this world, we may come to think of small-TAM software producers more as “creators” than as companies. A single person can do it, and many of them will. It could be fun and meaningful work, but it won’t be a great business model. It will be hyper-competitive and have a high failure rate, with a strong power-law distribution, meaning only a small number break through and generate real profits.

The need for distribution will ensure that even if there is fragmentation at the producer level, there will be ever steeper concentration at the platform level.

Turning non-software into software

AI will also drive the concentration of currently non-software industries. Perhaps the most dramatic example here will be in the services, which are highly fragmented today. In the US, there are 1.2M consulting firms, 400K law firms, and 85K accounting firms.

They are fragmented because (1) there are limited returns from scale and (2) the transaction costs to hire them on the open market are low: their services are discrete, well understood, and easy to price.

But if you’re not just renting out time but instead building agents that can do the work autonomously, that “returns from scale” dial gets turned way up. It’s a race to aggregate as much data and as many completed jobs as possible to enable a product that can do more work at higher accuracy and lower cost.

In our accounting example above, an automated services firm could reduce the cost of serving the marginal customer to close to zero. And as the data model grows, it would get faster and less error-prone across any type of customer and edge case.

This is the kind of company that Julien Bek wrote about in his excellent piece Services: The New Software:

“A company might spend $10K a year for QuickBooks and $120K on an accountant to close the books. The next legendary company will just close the books.”

Admittedly, tax prep is a bullseye use case because it has an agreed-upon set of rules, and the outputs are verifiably accurate - that is why many people are using it. But when you start to dig into the services, you find many other examples that look similar: claims adjusting, underwriting, paralegal, payroll processing, and regulatory and compliance, to name a few.

Automated services companies will get massive, and in doing so, begin to consolidate the fragmented services landscape we see today.

We’ll see AI’s centralizing effects across a much wider range of industries than we’ve discussed here. We haven’t even covered anything that touches the physical world, for example: industrials, transportation, manufacturing. AI can also be a centralizing force in these industries, particularly when paired with robotics.

The lesson of history is that new technology leads to more concentration, and AI has the potential to be the most powerful example of this yet.

This will not be an incremental change. As every major new technology before it has done, AI will produce companies that are so large they make the last generation look quaint.

End note

This essay is meant to be descriptive, not normative. I’m not saying it’s a good thing that we’ll see greater concentration, just that it is likely to happen. There are many benefits from centralization - the last wave of super companies produced unparalleled consumer surplus. But it also risks disrupting small business owners, contributing to economic inequality, and driving political unrest and a policy response that could be destructive.

It is worth noting, however, that the study we cited earlier also found that increasing business concentration has not necessarily led to greater inequality, in part because the ownership of companies has also become more diffuse over the same period. This is one reason to hope that companies like OpenAI and Anthropic get public quickly.

From the study:

Interestingly, across the countries and time periods in our sample, rising concentration of production activities is not necessarily accompanied by rising inequality among households, which suggests that their determinants can be different.

Although production has become more concentrated, ownership appears to become more diffuse over time: large companies used to be owned primarily by individuals and families; now, a broader group of households own their equity through investment funds and retirement savings.

Some people are making the inverse transaction cost argument about AI: agents will just transact on a user or company’s behalf and choose the supplier that is best for them, effectively collapsing transaction costs between companies and resulting in a much more fragmented market. For example, this is what the Citrini paper argued about DoorDash:

“A competent developer could deploy a functional competitor in weeks, and dozens did, enticing drivers away from DoorDash and Uber Eats by passing 90-95% of the delivery fee through to the driver. Multi-app dashboards let gig workers track incoming jobs from twenty or thirty platforms at once, eliminating the lock-in that the incumbents depended on. The market fragmented overnight and margins compressed to nearly nothing.”

The problem with this argument is that power still matters. If the market were fragmented, all of the suppliers would be sub-scale. They would have no network, no scale of operations, no shared data model. There would be no one to control quality or issue refunds. These products would be more expensive and lower quality, and would fail to earn market share.

I’ve seen many estimates of this number, ranging from about 100 to about 500. This one seems relatively reliable and is from https://productiv.com/blog/it-saas-statistics/. Regardless, it’s a big number.

I really appreciate your writing. I find it to be a reasonable/balanced view into the future. Keep it coming.

Love this. It flips the usual “AI will create infinite niche SaaS” take on its head and actually lines up with how power has shifted in every previous tech wave.

The bit that really jumps out to me is the services angle: once “renting time” turns into “renting an agent that just does the work,” you don’t just get consolidation, you get something closer to a few giant “operating systems for work” that sit underneath whole categories like accounting, claims, or compliance. It makes me wonder if, for a lot of founders, the real question isn’t “What company am I building?” so much as “Which future super-company am I quietly becoming a feature of, and can I live with that?”.